Coal Use in Thailand: Scale, Sources, and Sectors การใช้ถ่านหินในประเทศไทย: ปริมาณ แหล่งที่มา และการใช้งานในภาคส่วนต่างๆ

– อ่านบทความภาษาไทยด้านล่าง –

Coal Use in Thailand: Scale, Sources, and Sectors

Thailand’s energy landscape remains heavily influenced by coal, a fossil fuel that continues to play a significant role despite growing global momentum toward cleaner energy sources. Understanding how much coal Thailand uses, where it comes from, and how it is applied across different sectors provides crucial insight into the country’s energy challenges and opportunities. This article paints a vivid picture of coal’s role in Thailand’s economy and energy system, highlighting key facts and figures that reveal the complexity of balancing energy needs with environmental and social concerns.

The Scale of Coal Use in Thailand

As of 2022, Thailand’s total installed power generation capacity stood at approximately 47.2 gigawatts (GW). Coal accounted for about 9.8% of this capacity, roughly 4.6 GW, marking a notable reduction from 18.1% in 2010. This decline reflects a gradual but cautious shift toward renewable energy and cleaner alternatives. Renewable sources, including hydropower, now make up about 21.8% of the installed capacity, signaling a growing diversification of Thailand’s energy mix.

In terms of electricity production, coal-fired power plants generated around 36.5 terawatt-hours (TWh) in 2022, contributing nearly 20% of the country’s total electricity output. Between 2015 and 2021, Thailand’s coal consumption remained relatively stable, fluctuating between 37 and 39 million tons annually. However, domestic coal production has been declining, with only about 16.34 million tons produced locally. This gap has been increasingly filled by imports, which made up over 60% of Thailand’s coal demand in 2021, primarily sourced from Indonesia.

Where Does Thailand’s Coal Come From?

Thailand’s only active coal mine is located in Mae Moh, Lampang Province, in the country’s northwest. This lignite mine, operated by the Electricity Generating Authority of Thailand (EGAT), has been the backbone of the country’s coal supply since 1951. The Mae Moh mine holds the largest lignite reserves in Thailand and is expected to sustain mining operations for approximately 25 more years at current extraction rates.

The coal extracted from Mae Moh primarily fuels the Mae Moh thermal power plant, which has an installed capacity of about 2,455 megawatts (MW). This plant supplies roughly half of northern Thailand’s electricity, 30% of the central region’s, and 20% of the northeast’s. The importance of this coal source to regional energy security cannot be overstated.

However, domestic production alone cannot meet Thailand’s coal needs. The country imports significant quantities of coal, mainly from Indonesia, Australia, Russia, and Laos. These imports serve both the industrial sector and private power producers, reflecting Thailand’s reliance on international coal markets to sustain its energy demands.

How Is Coal Used in Thailand?

Coal in Thailand is primarily used in two sectors: electricity generation and industry.

- Electricity Generation

Coal-fired power plants remain a key pillar of Thailand’s electricity system. As of 2023, there are 13 coal-fired power plants across the country, with a total installed capacity of approximately 6,883 MW and contracted capacity of about 6,040 MW. EGAT’s Mae Moh plant is the largest, consuming around 14 million tons of lignite annually to generate electricity.

Plans are underway to reduce Mae Moh’s capacity to about 1,200 MW by 2026 and eventually close the plant by 2050. To ease this transition, EGAT aims to introduce biomass co-firing—initially blending 14% biomass with coal, with the goal of eventually using 100% biomass fuel. This strategy could help reduce coal consumption while maintaining energy supply stability.

Private sector players also contribute to coal-based electricity generation. Global Power Synergy Public Company Limited (GPSC) operates three coal-fired plants totaling around 660 MW, supplying electricity to EGAT and industrial users, particularly in the Map Ta Phut Industrial Estate. Other companies like TPI Polene Power and IRPC operate smaller coal-fired plants, with capacities of 150 MW and 307 MW respectively, often combined with natural gas-fired units.

- Industrial Use

While coal’s role in electricity generation is significant, the industrial sector has become an even larger consumer of coal in Thailand. Industries such as cement manufacturing, ceramics, and steel production rely heavily on coal both as a fuel and as a raw material.

The cement industry, in particular, is a major driver of coal demand, accounting for approximately 35% of total coal consumption. In 2023, the sector used about 1.28 million tons of coal fly ash—a byproduct of coal combustion from power plants like Mae Moh—as a substitute material in cement production. Despite efforts to adopt alternative fuels, coal remains the primary energy source for cement manufacturing.

Other industries, including textiles, food processing, paper, and fiber production, also use coal to generate the heat necessary for various manufacturing processes. This diversification of coal use underscores its entrenched role in Thailand’s industrial economy.

Coal Imports and Trends

Thailand’s coal imports have grown substantially in recent years, reflecting the country’s declining domestic production and steady demand. In 2023, imports totaled approximately 18 million tons. Of this, about 11.2 million tons were used by the industrial sector, 4 million tons by independent power producers (IPPs), and 2.8 million tons by small power producers (SPPs).

Major importers include Banpu Public Company Limited, which sources coal from Indonesia, China, and Australia, primarily supplying the paper industry and IRPC’s power plants. Banpu currently imports around 1 million tons annually but plans to reduce this to 500,000 tons in the future. Lanna Resources Public Company Limited imports 700,000 to 900,000 tons per year, mainly for the cement industry.

Historical data from the Energy Policy and Planning Office (EPPO) shows fluctuations in coal use in the industrial sector: 16.2 million tons in 2021, a drop to 2.9 million tons in 2022, and a rebound to 11.2 million tons in 2023. These variations reflect shifting industrial demands and market conditions.

The Socioeconomic and Environmental Context

Coal mining and use in Thailand, especially in Lampang Province, have deep socioeconomic implications. Approximately 9,000 jobs are directly linked to coal mining and coal-fired power generation in the Mae Moh area. Coal contributes about 18.1% to Lampang’s Gross Regional Domestic Product (GRDP) and 2.5% to the national GDP.

However, coal mining has also caused significant environmental degradation, including air and water pollution, deforestation, and land subsidence. Social conflicts have arisen due to displacement, health issues, and concerns over human rights. Around 30,000 people were displaced during the expansion of the Mae Moh power plant, highlighting the social costs of coal development.

Indigenous communities in the region face systemic challenges related to education, healthcare, and economic opportunities, exacerbated by the environmental impacts of coal mining.

Conclusion: A Complex but Critical Energy Reality

Coal remains a vital, though increasingly contested, component of Thailand’s energy and industrial sectors. It fuels a significant portion of the country’s electricity generation and underpins key industries like cement manufacturing. Domestic production from Mae Moh supports regional energy needs, but imports fill the growing gap between supply and demand.

Thailand’s coal use presents a complex balancing act: maintaining energy security and economic growth while addressing environmental degradation and social impacts. As the country moves toward a cleaner energy future, understanding the scale, sources, and uses of coal is essential for crafting effective policies that ensure a just and sustainable transition.

The story of coal in Thailand is one of deep-rooted reliance and emerging transformation; a narrative that will shape the nation’s energy landscape and environmental health for decades to come.

การใช้ถ่านหินในประเทศไทย: ปริมาณ แหล่งที่มา และการใช้งานในภาคส่วนต่างๆ

ประเทศไทยยังคงพึ่งพาถ่านหินเป็นแหล่งพลังงานสำคัญ แม้ว่าจะมีการเปลี่ยนผ่านไปสู่พลังงานสะอาดมากขึ้นก็ตาม ข้อมูลล่าสุดจากปี 2022-2023 แสดงให้เห็นภาพรวมการใช้ถ่านหินในประเทศอย่างชัดเจน ทั้งในแง่ของปริมาณที่ใช้ แหล่งที่มา และภาคส่วนที่นำถ่านหินไปใช้ประโยชน์ โดยบทความนี้จะช่วยให้ผู้อ่านเห็นภาพรวมที่เข้าใจง่ายและครบถ้วน

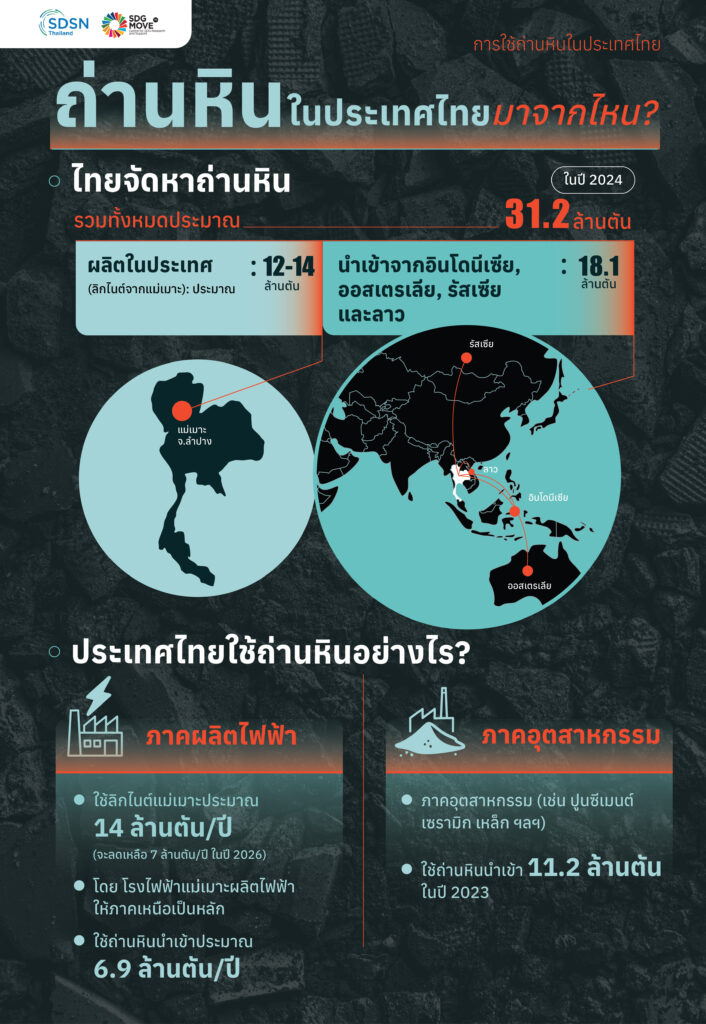

ปริมาณการใช้ถ่านหินในประเทศไทย

ในปี 2022 ประเทศไทยมีความจุการผลิตไฟฟ้าติดตั้งรวมประมาณ 47.2 กิกะวัตต์ (GW) โดยถ่านหินเป็นแหล่งพลังงานที่สำคัญเป็นอันดับสอง รองจากก๊าซธรรมชาติ โดยถ่านหินคิดเป็นสัดส่วนประมาณ 9.8% หรือประมาณ 4.6 GW ของกำลังการผลิตไฟฟ้าทั้งหมด ซึ่งลดลงจากประมาณ 18.1% ในปี 2010 แสดงให้เห็นว่าประเทศไทยเริ่มมีการเปลี่ยนผ่านไปสู่พลังงานสะอาดมากขึ้น แต่ถ่านหินยังคงเป็นส่วนหนึ่งของระบบพลังงานอย่างมีนัยสำคัญ

ในปี 2022 การผลิตไฟฟ้าจากถ่านหินอยู่ที่ประมาณ 36.5 เทระวัตต์ชั่วโมง (TWh) หรือคิดเป็นสัดส่วน 19.6% ของการผลิตไฟฟ้าทั้งหมดในประเทศ ปริมาณถ่านหินที่ใช้ในช่วงปี 2015-2021 อยู่ในระดับคงที่ประมาณ 37-39 ล้านตันต่อปี โดยการผลิตถ่านหินในประเทศลดลงเหลือประมาณ 16.34 ล้านตัน ส่งผลให้การนำเข้าถ่านหินเพิ่มสูงขึ้น โดยในปี 2021 การนำเข้าถ่านหินคิดเป็นมากกว่า 60% ของความต้องการถ่านหินทั้งหมด และส่วนใหญ่มาจากประเทศอินโดนีเซีย

แหล่งที่มาของถ่านหินในประเทศไทย

ประเทศไทยมีเหมืองถ่านหินหลักเพียงแห่งเดียว คือ เหมืองแม่เมาะในจังหวัดลำปาง ซึ่งเป็นเหมืองลิกไนต์ที่ใหญ่ที่สุดในประเทศ เหมืองนี้ดำเนินการโดยการไฟฟ้าฝ่ายผลิตแห่งประเทศไทย (กฟผ.) และคาดว่ายังมีถ่านหินสำรองเพียงพอสำหรับการทำเหมืองต่อไปอีกประมาณ 25 ปี

ถ่านหินจากเหมืองแม่เมาะส่วนใหญ่ใช้เป็นเชื้อเพลิงในโรงไฟฟ้าถ่านหินแม่เมาะ ที่มีกำลังการผลิตติดตั้งประมาณ 2,455 เมกะวัตต์ โรงไฟฟ้าแห่งนี้จ่ายไฟฟ้าให้กับภาคเหนือประมาณ 50% ภาคกลาง 30% และภาคตะวันออกเฉียงเหนือ 20% ของความต้องการไฟฟ้าในแต่ละภูมิภาค

นอกจากถ่านหินจากเหมืองแม่เมาะแล้ว ประเทศไทยยังต้องนำเข้าถ่านหินจากต่างประเทศเป็นจำนวนมาก โดยเฉพาะจากอินโดนีเซีย ออสเตรเลีย รัสเซีย และสปป.ลาว การนำเข้าถ่านหินส่วนใหญ่ถูกใช้ในภาคอุตสาหกรรมและโรงไฟฟ้าเอกชน

การใช้ถ่านหินในภาคส่วนต่างๆ

ถ่านหินในประเทศไทยถูกนำไปใช้ในสองภาคส่วนหลัก ได้แก่

1. การผลิตไฟฟ้า

ถ่านหินเป็นเชื้อเพลิงหลักในการผลิตไฟฟ้าของประเทศ โดยในปี 2023 กฟผ. มีโรงไฟฟ้าถ่านหินทั้งหมด 13 แห่ง รวมกำลังการผลิตติดตั้งประมาณ 6,883 เมกะวัตต์ และกำลังการผลิตที่สัญญารับซื้อไฟฟ้าประมาณ 6,039 เมกะวัตต์

โรงไฟฟ้าแม่เมาะเป็นโรงไฟฟ้าถ่านหินที่ใหญ่ที่สุดในประเทศ ใช้ถ่านหินลิกไนต์จากเหมืองแม่เมาะประมาณ 14 ล้านตันต่อปี แต่มีแผนลดกำลังการผลิตลงเหลือประมาณ 1,200 เมกะวัตต์ในปี 2026 และปิดโรงไฟฟ้าอย่างสมบูรณ์ในปี 2050 โดยจะเริ่มใช้เชื้อเพลิงชีวมวลร่วมกับถ่านหิน (Biomass Co-Firing) เพื่อช่วยลดการใช้ถ่านหินในระยะเปลี่ยนผ่าน

นอกจากกฟผ. ยังมีโรงไฟฟ้าเอกชน เช่น Global Power Synergy Public Company Limited (GPSC) ที่มีโรงไฟฟ้าถ่านหิน 3 แห่ง รวมกำลังการผลิตประมาณ 660 เมกะวัตต์ และบริษัทอื่นๆ เช่น TPI Polene Power และ IRPC ที่มีโรงไฟฟ้าถ่านหินขนาดเล็กในระบบของตนเอง

2. ภาคอุตสาหกรรม

นอกจากการผลิตไฟฟ้าแล้ว ถ่านหินยังถูกใช้ในภาคอุตสาหกรรมโดยเฉพาะในอุตสาหกรรมปูนซีเมนต์ ซึ่งเป็นผู้ใช้ถ่านหินรายใหญ่ที่สุดในภาคอุตสาหกรรม โดยใช้ถ่านหินประมาณ 35% ของปริมาณถ่านหินทั้งหมดที่ใช้ในประเทศ

ในปี 2023 อุตสาหกรรมปูนซีเมนต์ใช้ถ่านหินประมาณ 1.28 ล้านตันในรูปของ “coal fly ash” ซึ่งเป็นของเสียจากการเผาไหม้ถ่านหินที่นำมาใช้แทนส่วนหนึ่งของปูนซีเมนต์ ช่วยลดการใช้ปูนซีเมนต์จริงและลดผลกระทบต่อสิ่งแวดล้อม

นอกจากนี้ ถ่านหินยังถูกใช้ในอุตสาหกรรมอื่นๆ เช่น อุตสาหกรรมเครื่องปั้นดินเผา อุตสาหกรรมเหล็ก และอุตสาหกรรมที่ต้องใช้ความร้อนสูงในกระบวนการผลิต

แนวโน้มการใช้ถ่านหินและการนำเข้า

แม้ว่าการใช้ถ่านหินเพื่อผลิตไฟฟ้าจะมีแนวโน้มลดลงเล็กน้อยในช่วงหลายปีที่ผ่านมา แต่การใช้ถ่านหินในภาคอุตสาหกรรมกลับเพิ่มขึ้น โดยเฉพาะในอุตสาหกรรมปูนซีเมนต์และอุตสาหกรรมอื่นๆ ที่ต้องใช้ความร้อน

ในปี 2023 ปริมาณถ่านหินนำเข้าของไทยอยู่ที่ประมาณ 18 ล้านตัน โดยแบ่งเป็นการใช้ในภาคอุตสาหกรรมประมาณ 11 ล้านตัน โรงไฟฟ้าเอกชนประมาณ 4 ล้านตัน และโรงไฟฟ้าขนาดเล็กประมาณ 2.7 ล้านตัน

การนำเข้าถ่านหินส่วนใหญ่ยังคงมาจากอินโดนีเซีย ซึ่งเป็นแหล่งถ่านหินที่สำคัญและมีราคาที่แข่งขันได้ นอกจากนี้ บริษัทไทยบางแห่ง เช่น Banpu และ Lanna Resources ยังนำเข้าถ่านหินจากจีนและออสเตรเลียเพื่อใช้ในอุตสาหกรรมและการผลิตไฟฟ้า

ผลกระทบและความท้าทาย

การใช้ถ่านหินในประเทศไทย แม้จะช่วยให้ระบบไฟฟ้ามั่นคงและรองรับความต้องการพลังงานที่เพิ่มขึ้น แต่ก็สร้างผลกระทบต่อสิ่งแวดล้อมและสุขภาพของประชาชน เช่น มลพิษทางอากาศและการทำลายระบบนิเวศในพื้นที่เหมืองถ่านหิน

ชุมชนในจังหวัดลำปางที่อยู่ใกล้เหมืองแม่เมาะได้รับผลกระทบจากฝุ่นละอองและมลพิษทางอากาศ รวมถึงปัญหาสุขภาพและการเปลี่ยนแปลงวิถีชีวิต นอกจากนี้ การขุดเหมืองยังทำให้เกิดการทรุดตัวของพื้นที่และผลกระทบต่อชุมชนดั้งเดิม เช่น ชนเผ่ามลาบรีและกะเหรี่ยง

อย่างไรก็แล้วแต่ ถ่านหินยังคงเป็นแหล่งพลังงานสำคัญของประเทศไทย โดยใช้ในภาคการผลิตไฟฟ้าและภาคอุตสาหกรรม โดยเฉพาะอุตสาหกรรมปูนซีเมนต์ที่ใช้ถ่านหินอย่างมาก แม้ว่าจะมีการลดสัดส่วนการใช้ถ่านหินในระบบไฟฟ้า แต่ความต้องการถ่านหินในภาคอุตสาหกรรมยังคงสูงและมีแนวโน้มเพิ่มขึ้น

ประเทศไทยต้องเผชิญกับความท้าทายในการบริหารจัดการการใช้ถ่านหินอย่างยั่งยืน ทั้งในแง่ของการรักษาความมั่นคงทางพลังงานและการลดผลกระทบต่อสิ่งแวดล้อมและชุมชน การวางแผนและนโยบายที่เหมาะสมจึงเป็นสิ่งจำเป็น เพื่อให้การใช้ถ่านหินในอนาคตสอดคล้องกับเป้าหมายการพัฒนาที่ยั่งยืนและการเปลี่ยนผ่านสู่พลังงานสะอาดอย่างแท้จริง.